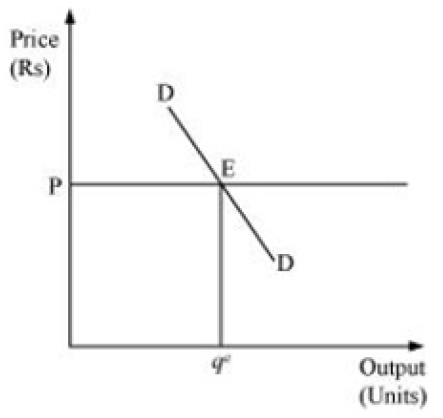

In the long run, due to the free entry and exit of firms, all the firms earn zero economic profit or normal profit. They neither earn abnormal profits nor abnormal losses. Thus, the free entry and exit feature ensures that in the long run the equilibrium price will be equal to the minimum of average cost, irrespective of whether profits or losses are earned in the short run.

The equilibrium is determined by the intersection of consumers' demand curve and the 'P = min AC' line. At equilibrium point E, quantity supplied by each firm is qe at the price (P).