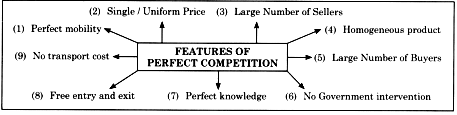

(1) Perfect Mobility of Factors of Production : Factors of production that is land, labour, capital are perfectly free to move from one firm to another or from one industry to another from one region to another or from one occupation to another. This ensures freedom of entry and exit for individuals and firms.

(2) Single / Uniform Price : There exists a single price for homogeneous product in the entire market at a given point of time. The price is determined by forces of demand and supply.

(3) Large Numbers of ellers : There are many sellers in this market. The number of sellers (firms) are so large that a single seller cannot influence the market price nor the total output in the market (Industry). The contribution of one seller is insignificant and microscopic. The price in the market is determined by the forces of market demand and market supply. Hence, a firm or seller is a 'price taker'and not a 'price maker.'

(4) Homogeneous Product : The products produced by all the firms in the industry are identical and are perfect substitute to each other. The products are identical in shape, size, colour, etc. and hence uniform price rules the market for the product.

(5) Large Number of Buyers : There are large number of buyers in the market. One individual buyer’s demand is only a small fraction of total market demand so he is not in a position to influence the price. He is a price taker.

(6) No Government Intervention : It is assumed that the government does not interfere with the working of market economy.

There are no tariffs, subsidies, licensing policy or other government interventions. This non – intervention of government is necessary to permit free entry of firms and automatic adjustment of demand and supply. In short, laissez faire policy prevails under perfect

(7) Perfect Knowledge : There is perfect knowledge on the part of buyers and sellers regarding the market conditions especially regarding market price. As a result no buyer will pay a higher price than the market price and no seller will charge a lower price than the market price. So a single price would prevail for a commodity in the entire market.

(8) Free Entry and Free Exit : There is freedom for new firms or sellers to enter the industry or market. There are no legal, j economic or any other type of restrictions or; barriers for new firms to enter the industry or an existing firms to quit the industry, Entry of new firm usually takes place j when existing firms enjoy abnormal profit. Similarly, existing firms quit the industry when they face losses.

(9) No Transport Cost : It is assumed that all firms are close to the market and hence there is no transport cost. If the transport cost are added to the price of product then the homogeneous commodity will have different prices depending upon the distance from the place of supply to the market.